Zhou Liying, 29, a marketing specialist at an international company in Beijing, is thinking about transferring her money from a wealth management product to fixed deposits in the hope of getting a higher return after the central bank raised the limit placed on deposit interest rates.

|

|||

But the returns on such products are declining as the rate of inflation decreases and monetary policies are loosened, analysts and banking executives said.

Such wealth products are often issued by commercial lenders and require a minimum investment of 50,000 yuan ($7,860). The capital thus raised often goes to buying bonds, making loans and financing company projects.

A supervisor surnamed Li, with the Bank of China Ltd's wealth management sector, said the sales prospects for wealth products remain good in the first half of the year compared with the same period of last year. Even so, the returns have been declining, especially after the first quarter.

According to statistics from Wind Information Co Ltd, commercial lenders in China issued 11,530 wealth products in the first five months of the year, up by 34 percent from the 8,619 products issued during the same period last year.

"But this year, the returns on wealth products have shown obvious consecutive declines and big monthly drops," said Chengdu-based Fanhua Puyi Investment Management Co Ltd in a research note.

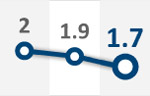

The expected returns on products issued last month decreased by 21 basis points from what they were in April, and their average maturities were shortened by seven days, falling to 123 days, according to data collected by Fanhua Puyi.

Between June 1 and 7, the expected returns on yuan-denominated products stood at 4.6 percent on average, down by 0.2 percentage point from May and 0.4 percentage point from April, it said.

Wu Ningjiang, an analyst at Fanhua Puyi, said the returns on wealth products will probably continue to fall following the People's Bank of China's decision to reduce interest rates on June 8.

The central bank also allowed lenders to price their deposit rates for the first time at 1.1 times the benchmark deposit rates.

"Since May, liquidity has continued to loosen, which will further cool down the returns on such products," Wu said. "Selling wealth products was a 'powerful' means that banks had of collecting deposits, therefore the expected returns on these products are related closely to how much the banks want to get from deposits."

"Given that there might be another two interest rates cuts at the most in the next half a year, a number of wealth management clients will prefer fixed deposits," Li said.

"But generally speaking, the fever for wealth products will not pass away soon. Clients don't have many alternatives to striking a balance between obtaining sound returns and having enough liquidity. Moreover, banks are improving these products to make them more suitable to current conditions."

Li said the most popular products among clients now are those that have maturities of between six months and a year. The most popular products last year had maturities of less than a month.

The financial system may come under greater risk as banks' wealth management businesses rapidly expand and take on more off-balance sheet assets, which remain insufficiently transparent, said May Yan, director of Barclays Capital Asia and a banking analyst.

"The regulation of such products must be strengthened, as it's usually very difficult to learn details about where such money is being invested."

In addition, wealth products tend to have short maturities even though the money they raise often goes into long-term projects. That situation gives rise to huge risks, Yan said.

The China Banking Regulatory Commission tightened its reins on these products in July 2011, prohibiting banks from buying each other's products. It also urged lenders to take steps to control credit risks that stem from projects related to roads and railways.

Later, in November, it suspended sales of wealth products with maturities of less than a month.

By the end of last year, the amount of assets in wealth products had increased to 5.5 trillion yuan, the equivalent of 7 percent of deposits, up from less than 4 percent a year earlier, the Wall Street Journal cited Simon Ho, China bank expert at Citigroup Inc, as saying.

For more subscription details of China Banking, please visit our E-Shop.

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()